US-Germany Trade Relations 2024-25: US Tariffs on Germany & Bilateral Trade Data

Explore US-Germany trade relations in 2025, including US tariffs on Germany, major German exports to the US & key US Germany bilateral trade data.

Introduction

Few bilateral relationships shape the global trading system as much as that between the United States and Germany. Together, they represent two of the world’s largest, most advanced economies, each deeply integrated into global value chains & manufacturing networks. For decades, their trade relationship has been defined by mutual dependence: Germany’s industrial exports flow into the U.S. market, while American technology, energy, & financial services play central roles in Germany’s economy. According to the latest US import data and Germany export data, the total value of US imports from Germany reached $163.54 billion in 2024 and $81.03 billion in the first two quarters of 2025. The total value of US exports to Germany accounted for $75.61 billion in 2024 and $41.32 billion in the first two quarters of 2025, as per the US export data & US-Germany trade statistics. Import car from Germany to US remains popular among enthusiasts seeking high-performance vehicles, even as questions like what does Germany import from the US highlight the broader two-way flow of goods between the countries.

Top 10 US Imports from Germany: What Does the US Import From Germany?

The top 10 US imports from Germany consist of various goods that contribute significantly to trade between the two countries. Machinery, vehicles, pharmaceuticals, optics, and measurement devices are among the key imports from Germany to the United States. Germany's precision engineering and high-quality manufacturing are reflected in the imports of vehicles such as luxury cars and parts for industrial machinery. These goods not only strengthen the economic ties between the two nations but also showcase the expertise and innovation of German industries. The top 10 goods that the US imports from Germany, as per the US shipment data and the US-Germany import trade data for 2024-25, include:

1. Vehicles (HS code 87): $34.87 billion

Germany is renowned for its automotive industry, with brands like BMW, Mercedes-Benz, and Volkswagen dominating the market. It's no surprise that vehicles are the top US import from Germany, as per the data on US vehicle imports from Germany by HS code. From luxury cars to commercial vehicles, Germany's automotive sector plays a significant role in the country's export economy.

2. Nuclear reactors & machinery (HS code 84): $34.34 billion

Another substantial import category from Germany is nuclear reactors and machinery. Germany has a strong engineering and manufacturing base, producing high-quality machinery and equipment that is in demand globally. The US relies on Germany for a variety of industrial machinery to support its own manufacturing sector.

3. Pharmaceutical products (HS code 30): $17.21 billion

Germany is home to several pharmaceutical giants, producing a wide range of medications and healthcare products. The US imports a significant amount of pharmaceutical products from Germany, reflecting the quality and innovation present in the German healthcare industry.

4. Optical, medical, & surgical instruments (HS code 90): $13.68 billion

Germany is known for its precision engineering and advanced medical technology. The US imports a substantial amount of optical, medical, and surgical instruments from Germany, relying on the country's expertise in this field to support its healthcare system.

5. Electrical machinery & equipment (HS code 85): $11.98 billion

Electrical machinery and equipment are crucial imports from Germany for the US. From electronics to industrial equipment, Germany produces a wide range of electrical products that are in demand globally. The US imports a significant amount of electrical machinery and equipment from Germany to support various industries.

6. Aircraft, spacecraft, & parts thereof (HS code 88): $5.50 billion

Germany's aerospace industry is another significant player in the global market. The US imports aircraft, spacecraft, and parts thereof from Germany to meet its own aviation needs. Germany's expertise in aerospace technology makes it a reliable source for high-quality aircraft and components.

7. Plastics and articles thereof (HS code 39): $3.90 billion

Plastics are a ubiquitous material used in various industries, from packaging to construction. Germany is a leading producer of plastics and articles thereof, supplying the US with a substantial amount of plastic products. The US relies on Germany for high-quality plastics to meet its manufacturing needs.

8. Miscellaneous chemical products (HS code 38): $3.27 billion

Germany is known for its chemical industry, producing a wide range of chemical products for various applications. The US imports miscellaneous chemical products from Germany, including specialty chemicals and raw materials. Germany's expertise in chemical manufacturing makes it a valuable trade partner for the US.

9. Organic chemicals (HS code 39): $2.80 billion

Organic chemicals are essential raw materials used in various industries, from pharmaceuticals to agriculture. Germany produces a significant amount of organic chemicals, which are imported by the US for manufacturing purposes. The US relies on Germany for high-quality organic chemicals to support its industries.

10. Articles of iron or steel (HS code 73): $2.67 billion

Iron and steel are foundational materials used in construction, manufacturing, and infrastructure projects. Germany produces a substantial amount of articles of iron or steel, which are imported by the US for a variety of applications. The US relies on Germany for quality iron and steel products to meet its industrial needs.

Top 10 US Exports to Germany: What does the US Export to Germany?

The United States has a robust trade relationship with Germany, with a diverse range of exports making their way across the Atlantic. Some of the top US exports to Germany include motor vehicles, aircraft and spacecraft parts, pharmaceutical products, machinery, and electrical machinery. This bilateral trade between the US and Germany highlights the mutual economic benefit and close partnership shared between the two nations. The top 10 goods that the US exports to Germany, as per the US trade data and data on the US exports to Germany by HS code, for 2024-25, include:

1. Aircraft, spacecraft, & parts thereof (HS code 88): $9.57 billion

Aircraft, spacecraft, and their components have been a lucrative export category for the US. Germany, with its advanced aerospace industry, has a constant demand for high-quality aircraft and parts. The US has established itself as a reliable supplier in this sector, contributing significantly to its export revenue.

2. Vehicles (HS code 87): $9.19 billion

The automotive industry is a cornerstone of both the US and German economies. As a result, the export of vehicles from the US to Germany has been substantial. Whether it's cars, trucks, or other types of vehicles, the US has a strong presence in the German market.

3. Pharmaceutical products (HS code 30): $7.67 billion

The healthcare sector is a priority for both the US and Germany, leading to a significant export of pharmaceutical products. With cutting-edge research and development, the US has been able to supply high-quality medications to meet the demand in the German market.

4. Nuclear reactors & machinery (HS code 84): $7.56 billion

The energy sector is another area where the US excels in exports to Germany. Nuclear reactors and machinery play a vital role in ensuring a stable energy supply, as per the data on US machinery exports to Germany by HS code. The US has been a key supplier of these products to support Germany's energy needs.

5. Optical, medical, or surgical instruments (HS code 90): $6.78 billion

Germany is renowned for its precision engineering and quality medical equipment. The US has capitalized on this by exporting a wide range of optical, medical, and surgical instruments to meet the demand in the German healthcare industry.

6. Mineral fuels & oils (HS code 27): $6.55 billion

The US is a major producer of mineral fuels and oils, making it a significant exporter to Germany. As a country with a high energy consumption, Germany relies on imports to meet its energy requirements. The US has been a reliable source of these products over the years.

7. Electrical machinery & equipment (HS code 85): $6.17 billion

Electrical machinery and equipment have seen a surge in demand globally, including in Germany. The US has been at the forefront of innovation in this sector, exporting a diverse range of products to cater to the German market's needs.

8. Organic chemicals (HS code 29): $2.65 billion

Chemical products have a wide range of applications across various industries. Organic chemicals, in particular, have been a significant export category for the US to Germany. These products are essential for manufacturing processes and other applications in the German market.

9. Miscellaneous chemical products (HS code 38): $2.18 billion

In addition to organic chemicals, miscellaneous chemical products have also been in demand in Germany. The US has been able to meet this demand by exporting a variety of chemical products to support various industries in Germany.

10. Precious stones & metals (HS code 71): $1.82 billion

The export of precious stones and metals has been a niche yet lucrative market for the US in Germany. With a reputation for quality and craftsmanship, the US has been able to supply precious stones and metals to meet the demand in the German market.

The Policy Shift: From Targeted Tariffs to a Reciprocal Trade Regime

The backdrop

Trade friction between the U.S. and the European Union has existed for decades, but the modern cycle began in 2018 with American tariffs on steel and aluminum under Section 232 of the Trade Expansion Act. Germany, Europe’s largest industrial exporter, was among the hardest hit. Though the EU and U.S. later negotiated a tariff-rate quota system to ease tensions, the underlying suspicion of European trade surpluses persisted in Washington.

In recent years, US tariffs on Germany have significantly impacted the dynamics of US-German trade, raising concerns about long-term stability in US trade with Germany. As Germany exports to USA a wide range of goods, most notably automobiles, machinery, and pharmaceuticals, the widening US-Germany trade deficit has become a central issue in economic discussions. The US-Germany trade balance continues to reflect a substantial surplus in Germany’s favor, prompting a reassessment of US Germany trade relations. Analysts frequently ask, what does Germany export to the US and what does the US export to Germany, as trade patterns shift due to policy changes.

Germany major exports to the US, including vehicles and industrial equipment, underscore the importance of Germany trade with US in sustaining its export-driven economy. With the Germany US trade surplus reaching record highs, policymakers have debated the need for a new Germany US trade agreement to restore balance and encourage reciprocal market access.

By 2024, that suspicion was back at the center of U.S. trade policy. With Germany’s trade surplus with the U.S. hitting roughly €70 billion (about USD 76 billion) that year, the largest bilateral surplus in decades, the political case for “reciprocal tariffs” gained traction. The argument: Germany’s export-driven model benefits from the U.S. consumer market while offering limited reciprocity for American goods.

The 2025 tariff escalation

In April 2025, the U.S. government formally introduced a “Reciprocal Tariff Program,” applying across-the-board duties on imports from trade partners with persistent surpluses against the United States. The European Union, and thus Germany, were immediately included.

The new framework was introduced:

-

A 10 % baseline tariff on nearly all EU-origin goods beginning April 5, 2025.

-

An escalation to 20 % from April 9 if no negotiated exemptions were reached.

-

Continued sectoral tariffs on steel (25 %), aluminum (10–15 %), and certain autos (up to 25 %).

These tariffs were additive, meaning existing duties remained in place. Effectively, a German car entering the U.S. could face a 25 % automotive tariff plus the new 10–20 % reciprocal duty, depending on classification.

Negotiation and adjustment

After months of economic turbulence, a partial U.S.–EU trade agreement was reached in late July 2025. The deal moderated the tariffs to 15% on most EU-origin goods and offered limited exemptions for critical sectors such as aerospace, medical devices, and select energy products. However, automotive exports remained subject to a combined duty of roughly 15–20 %, depending on the manufacturer’s local U.S. investment footprint.

The U.S. Trade Representative’s office confirmed that these new rates applied retroactively to shipments after August 1, 2025, which caused confusion and logistical strain for German exporters already struggling with margin compression and falling orders.

The outcome was clear: by mid-2025, the U.S. had entrenched a high-tariff regime for European and especially German exports, creating the most restrictive trade environment in transatlantic commerce since the 1980s.

Trade in Numbers: The 2024–25 Data Story

The 2024 baseline

According to both German and U.S. official data, 2024 marked a peak in transatlantic trade volumes before the downturn began.

-

Total US–Germany goods trade (exports + imports): approximately €253 billion (or about USD 270 billion).

-

U.S. exports to Germany: about USD 75.7 billion.

-

U.S. imports from Germany: around USD 160.4 billion.

-

U.S. trade deficit with Germany: roughly USD 84.7 billion.

Germany thus exported more than twice as much to the U.S. as it imported, one reason the U.S. administration singled it out for the reciprocal tariffs.

Germany’s export exposure to the U.S. was at a two-decade high. Roughly 10.4 % of total German exports went to the American market, surpassing China as Germany’s largest single export destination.

Monthly trends in 2025: US-Germany Trade Data 2025

The U.S. Census Bureau’s monthly trade data for US trade in goods with Germany in 2025 reveals how quickly the U.S.-Germany trade conditions deteriorated once tariffs were announced:

|

Month (2025) |

US Exports to Germany ($) |

US Imports from Germany ($) |

US Trade Balance (USD) |

|

January |

$6.09 billion |

$13.65 billion |

–7.56 billion USD |

|

February |

$5.96 billion |

$12.67 billion |

–6.71 billion USD |

|

March |

$8.12 billion |

$15.65 billion |

–7.52 billion USD |

|

April |

$7.34 billion |

$13.16 billion |

–5.82 billion USD |

|

May |

$6.46 billion |

$13.30 billion |

–6.83 billion USD |

|

June |

$7.32 billion |

$11.08 billion |

–3.76 billion USD |

|

July |

$6.55 billion |

$12.82 billion |

–6.27 billion USD |

By mid-2025, cumulative U.S. exports to Germany totaled USD 47.9 billion, while imports from Germany reached USD 92.4 billion, producing a year-to-date deficit of about USD 44.5 billion.

Two points stand out:

-

Imports from Germany fell sharply in June 2025, down more than USD 2 billion month-to-month, as U.S. buyers paused orders in anticipation of higher tariffs.

-

Exports from the U.S. to Germany remained relatively stable, reflecting ongoing demand for U.S. aerospace, tech, and energy products.

The asymmetry shows that the burden of adjustment fell squarely on German exporters.

Late 2025: The downturn deepens

By August and September 2025, Germany’s exports to the U.S. had fallen to their lowest level in four years. Compared with August 2024, exports to the U.S. were down nearly 20%, and total German exports across all destinations dropped around 5% year-on-year. In sectors like automotive and machinery, the decline exceeded 25%.

German export orders, an early indicator of manufacturing health, contracted for seven consecutive months through September 2025. Economists estimate that the tariff shock alone could shave 0.8–1.0 percentage points off Germany’s GDP growth in 2025, translating into tens of thousands of industrial job losses.

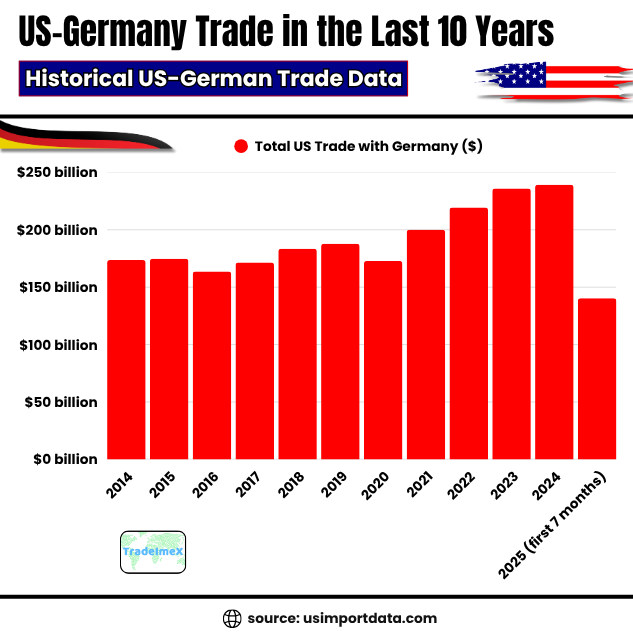

US-Germany Trade in the Last 10 Years: Historical US-German Trade Data

|

Year of Trade |

Total US Trade with Germany ($) |

|

2014 |

$173.59 billion |

|

2015 |

$174.85 billion |

|

2016 |

$163.65 billion |

|

2017 |

$171.49 billion |

|

2018 |

$183.46 billion |

|

2019 |

$187.85 billion |

|

2020 |

$172.89 billion |

|

2021 |

$200.01 billion |

|

2022 |

$219.47 billion |

|

2023 |

$235.85 billion |

|

2024 |

$239.15 billion |

|

2025 (first 7 months) |

$140.25 billion |

Where the Impact Hits Hardest

1. Automotive and parts

The automotive industry is the centerpiece of Germany’s export economy and the biggest casualty of the tariff escalation. In 2024, vehicles and auto parts accounted for nearly 30 % of Germany’s exports to the U.S., valued at over USD 45 billion.

The new 15–20 % tariffs on vehicles and components hit manufacturers like BMW, Mercedes-Benz, and Volkswagen directly. These companies already face thin profit margins on U.S.-bound exports due to logistics costs and emissions compliance. A tariff increase of that scale wipes out profitability on many models.

To mitigate the impact, German automakers have been negotiating with U.S. officials for relief in exchange for greater investment in American assembly plants. Some have pledged new or expanded operations in South Carolina, Alabama, and Tennessee, where they already employ thousands of U.S. workers. However, building new capacity takes years; short-term production cannot easily shift.

In the interim, many automakers are redirecting U.S.-bound production to Mexico and Eastern Europe, where parts of the supply chain may be reclassified to exploit different tariff codes or regional trade advantages under the USMCA framework. Still, this workaround only partially offsets the loss.

2. Machinery and capital goods

Germany’s industrial equipment exports, such as machine tools, pumps, turbines, and robotics, make up roughly 20 % of its U.S. exports. These products are highly specialized, often sold to American manufacturers as capital inputs. The new reciprocal tariffs raise costs for U.S. buyers and reduce German competitiveness relative to domestic or Asian suppliers.

Many German mid-sized firms (the Mittelstand) have limited ability to absorb tariffs or relocate production abroad. For them, the tariffs act as a direct squeeze on margins. Some are now considering partial production shifts to the U.S. to avoid duties, but financing and regulatory complexities make this a long process.

3. Chemicals and pharmaceuticals

Germany is also a major supplier of pharmaceuticals, specialty chemicals, and lab materials to the U.S., accounting for another 15 % of its exports. In this sector, tariff impacts are mixed: high-value patented products often face lower sensitivity, but commodity-grade chemicals and medical disposables are now significantly more expensive in the U.S. market.

Companies like Bayer, BASF, and Merck KGaA have large U.S. subsidiaries, which offer some insulation. However, exports from German facilities are still subject to the new duties. Some pharmaceutical firms have responded by rerouting shipments through U.S. affiliates, effectively “onshoring” inventory to minimize tariff exposure.

4. Steel, metals, and intermediate goods

The metals sector, long a friction point, faces cumulative tariff layers. Section 232 duties on steel and aluminum remain intact, and the new reciprocal tariffs apply on top. For some categories, this means effective import duties of 35-40 %, making many German-made components uncompetitive in U.S. manufacturing supply chains.

5. Indirect and supply-chain effects

Even firms not directly exporting to the U.S. are affected indirectly:

-

Input disruption: German manufacturers using U.S. parts or materials face cost fluctuations and longer lead times.

-

Investment deferrals: Many export-reliant firms have delayed expansion plans amid policy uncertainty.

-

Currency volatility: The euro’s moderate depreciation against the dollar provides limited relief but cannot offset the tariff burden.

Collectively, these factors amplify Germany’s broader industrial slowdown.

Economic and Strategic Fallout

Macroeconomic impact in Germany

By late 2025, Germany’s export-driven economy will be feeling the shock. Industrial output in August 2025 was down nearly 2% from the previous month and over 4% year-on-year, driven by weakness in autos, metals, and machinery. Business confidence indices dropped to their lowest levels since the pandemic.

Economic institutes in Berlin estimate that the tariff regime, if sustained through 2026, could reduce German GDP by roughly 1% and cost over 100,000 jobs in manufacturing. The pain is concentrated in export-heavy regions like Bavaria, Baden-Württemberg, and Lower Saxony.

The U.S. perspective

From the American side, the new tariffs are politically popular among certain constituencies but economically ambiguous. They may reduce the bilateral trade deficit in nominal terms, but they also raise costs for U.S. manufacturers and consumers. German autos, chemicals, and machinery are integral to U.S. supply chains, so tariffs act as a hidden tax on downstream industries.

For example, U.S. automakers that rely on German components now face higher input costs, while energy-intensive producers dependent on German machinery face supply delays. The macroeconomic benefit of rebalancing trade is therefore limited.

Diplomatic and legal dimensions

The European Union has prepared, but not fully implemented, retaliatory measures targeting American products such as bourbon, motorcycles, and agricultural exports. The EU’s approach is cautious, hoping to preserve negotiating room and avoid a full-scale trade war.

Legal challenges are also under discussion. Some EU officials argue that blanket reciprocal tariffs violate World Trade Organization rules, as they discriminate based on trade balances rather than specific unfair practices. However, the WTO’s dispute mechanism remains weakened, limiting the EU’s options for quick relief.

Corporate strategy: adapting under duress

German firms are employing several strategies to survive the tariff storm:

-

Localization: Expanding U.S.-based production to classify goods as domestic and bypass tariffs.

-

Diversification: Seeking alternative export markets in Asia, the Middle East, and Latin America to compensate for lost U.S. demand.

-

Hedging: Using financial instruments to manage exchange-rate and price volatility.

-

Supply-chain restructuring: Relocating intermediate stages of production to non-EU countries with more favorable trade access to the U.S.

These responses reflect a broader shift toward regionalized manufacturing networks, a trend that may persist even if tariffs are later reduced.

Outlook: Scenarios for 2026 and Beyond

Best-case scenario: Controlled normalization

Under an optimistic scenario, the U.S. and EU consolidate their July 2025 deal into a broader trade framework in 2026. Reciprocal tariffs could be reduced to single-digit levels, conditional on investment and market-access concessions. German exports might stabilize by mid-2026, with a modest recovery thereafter.

In this case, Germany’s GDP loss would remain limited to around 0.5%, and employment impacts could be partially offset by fiscal support and domestic investment.

Baseline scenario: Prolonged adjustment

The more likely path is one of slow adaptation. Tariffs stay near 15% through 2026, with partial exemptions negotiated sector by sector. German exporters adjust via localization and diversification, but total export volumes to the U.S. remain below 2023 levels. The bilateral trade imbalance narrows slightly but not dramatically.

Economic drag continues, with German industrial growth remaining weak and U.S. consumers absorbing higher prices for imported goods.

Worst-case scenario: Escalation to full trade war

If diplomatic negotiations collapse and tariffs climb to 25–30%, a true transatlantic trade war could emerge. Retaliatory EU tariffs would hit U.S. agricultural and tech exports, while German industries would see export volumes plunge by over 25%. Under this scenario, German GDP could contract by 1–1.5%, with widespread layoffs in manufacturing and trade.

The geopolitical consequences would be severe: weakening NATO cooperation, stalling climate initiatives, and undermining the global credibility of the Western economic alliance.

Conclusion: A Turning Point in Transatlantic Trade

In conclusion, the 2024–25 period marks a defining chapter in US–Germany trade relations. What was once a model of industrial complementarity has turned into a case study in economic confrontation. The U.S. tariffs introduced in 2025 are not minor adjustments; they represent a structural reset in how America engages with high-surplus partners like Germany. The numbers speak plainly: German exports to the U.S. are down by double digits, industrial output is slipping, and the once-stable trade surplus that anchored Germany’s growth is under threat. For American industries, meanwhile, the tariffs bring temporary protection but long-term uncertainty and higher costs.

Whether the relationship returns to cooperation or continues toward fragmentation will depend on choices made in 2026. If both sides pursue pragmatic, rules-based engagement, the damage can be contained. If not, the U.S.–Germany trade rift could become the defining economic fault line of the decade, reshaping global supply chains, eroding competitiveness, and testing the resilience of the transatlantic alliance itself.

We hope that you liked our data-driven and interactive blog report on the US-Germany trade relations & bilateral trade data 2025. For more insights into the latest US trade data, or to search live US import-export data by country, visit USImportdata. Contact us at info@tradeimex.in and get customized US trade reports, market insights, and the latest import-export database, as per your requirements.

Also read about:

What's Your Reaction?