US Iron Ore Import Data 2024-25: Top Iron Ore Importers & Buyers in USA

Explore detailed US iron ore import data for 2024-25, top iron ore importers & buyers in USA, key sourcing countries, & strategic trends shaping the U.S. steel industry.

Introduction

Iron ore is the essential input for steelmaking, and steel is the backbone of the U.S. industrial economy. From automotive to construction, from shipbuilding to energy infrastructure, American demand for steel shapes the demand for iron ore. While the United States possesses significant domestic iron ore reserves, mainly concentrated in Minnesota and Michigan, domestic production alone does not fully satisfy every segment of the U.S. steel industry. Iron ore is an essential raw material for the production of steel, making it a crucial component of various industries worldwide. According to the US import data and the iron ore import data of USA, the total value of US iron ore imports reached $834.20 million in 2024, a 7% decline from the previous year. In the first two quarters of 2025 or H1 2025, the US imported iron ores worth $432.81 million, as per the US iron ore import data. The U.S. relies on foreign supply for a significant share of its iron ore needs, which leads many to ask does the US import iron ore despite having domestic production.

Due to demand from steel manufacturers, how much iron ore does the US import becomes an important question for understanding supply chain trends and market dependence. Various iron ore buyers in USA, including major steel mills, manufacturing companies, and industrial processors, source iron ore from countries like Canada, Brazil, and Sweden to meet production requirements. According to the latest global trade data, the US is the 15th largest iron ore importer in the world. Iron ore Imports are required for certain high-grade ores, specific pellet types, or to balance cost and supply chain constraints. The years 2024 and 2025 are particularly interesting for the U.S. iron ore trade. They capture the intersection of three forces: the global realignment of commodity flows, the rise of electric arc furnace (EAF) steelmaking in America, and the renewed emphasis on supply chain security in critical minerals.

Looking at the import data gives a sharper view of where the U.S. sits in the global iron ore trade and who the real buyers are inside the country. In this article, we will explore the top iron ore importers and buyers in USA, with a key focus on the US iron ore import data for 2024-25.

The Scale of U.S. Iron Ore Imports

The United States, being a major player in the global steel market, heavily relies on importing iron ore to meet its domestic demand, as per the report on the United States iron ore industry. In global terms, the U.S. is a small player in raw iron ore imports. The world’s largest iron ore importers, China, Japan, South Korea, Germany, and Taiwan, buy tens of billions of dollars worth of iron ore annually. By contrast, U.S. imports of raw ore in 2024 totaled just under $835 million, accounting for less than one percent of global import value.

However, the raw number hides nuance. U.S. imports are small because the country produces a significant share of its own ore domestically. But the ore it does import tends to be:

-

High value per ton: The average landed cost for U.S. imports was among the highest in the world in 2024, close to $170 per ton, compared to global averages closer to $110–130 per ton.

-

Highly specific in grade and form: Imports often include high-grade fines, pellets, or direct reduction feedstock that U.S. mines cannot fully supply.

-

Linked directly to key steel producers: Unlike in China, where ore is dispersed across hundreds of buyers, U.S. imports are concentrated among a handful of large firms.

This means that while total volume is modest, the strategic importance of imports is outsized.

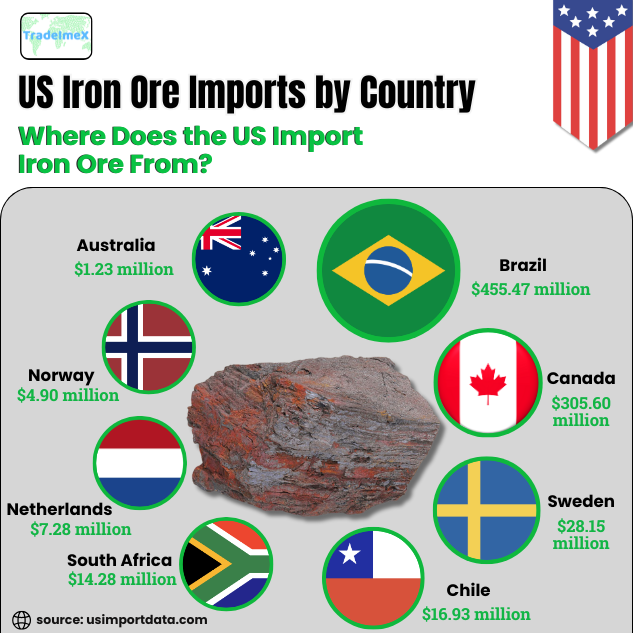

US Iron Ore Imports by Country: Where Does the US Import Iron Ore From?

In examining the top sources of iron ore imports for the United States, it is essential to consider the significant contributors to the country's iron ore supply chain. Historically, the leading countries supplying iron ore to the US include Australia, Brazil, Canada, and Sweden. These nations have played a crucial role in meeting the United States' demand for iron ore due to their rich reserves and efficient mining operations.

The consistent supply of high-quality iron ore from these top import sources has been vital in supporting various industries in the US, such as steel production & infrastructure development. The top 10 import partners of the US for iron ore imports, as per the US iron ore imports by country and the US shipment data for 2024-25, include:

1. Brazil: $455.47 million (4.91 million tons)

Brazil has long been a significant supplier of iron ore to the United States. In 2024-25, the US imported a whopping $455.47 million worth of iron ore from Brazil, accounting for 4.91 million tons. Brazil's rich iron ore reserves and efficient mining infrastructure make it a top choice for countries like the US that rely on imported iron ore.

2. Canada: $305.60 million (2.57 million tons)

Canada is another key player in the US iron ore import market, providing the US with $305.60 million worth of iron ore in 2024-25, equivalent to 2.57 million tons. The proximity of Canada to the US and its well-established mining industry make it a reliable source of iron ore for the United States.

3. Sweden: $28.15 million (1.81 million tons)

In 2024-25, the US imported $28.15 million worth of iron ore from Sweden, amounting to 1.81 million tons. Sweden's high-quality iron ore deposits and sustainable mining practices appeal to countries like the US that prioritize responsible sourcing of raw materials.

4. Chile: $16.93 million (184.28 thousand tons)

Chile may be a smaller player in the US iron ore import market, but it still contributed $16.93 million worth of iron ore to the United States in 2024-25, totaling 184.28 thousand tons. Chile's iron ore exports complement the diverse import sources that the US relies on to meet its iron ore needs.

5. South Africa: $14.28 million (121.09 thousand tons)

South Africa is another country that supplies iron ore to the United States, with imports totaling $14.28 million in 2024-25, equivalent to 121.09 thousand tons. South Africa's iron ore exports play a part in ensuring a steady supply of iron ore for the US steel industry.

6. Netherlands: $7.28 million (91 thousand tons)

The Netherlands may not be a traditional iron ore producer, but it still managed to export $7.28 million worth of iron ore to the United States in 2024-25, amounting to 91 thousand tons. The Netherlands' role in the US iron ore import market showcases the global nature of the iron ore trade.

7. Norway: $4.90 million (37.30 thousand tons)

Norway's contribution to the US iron ore import market may be relatively modest, but it still supplied $4.90 million worth of iron ore to the United States in 2024-25, totaling 37.30 thousand tons. Norway's participation highlights the diverse range of countries from which the US sources its iron ore.

8. Australia: $1.23 million (34.96 thousand tons)

Australia, known for its vast iron ore reserves and efficient mining operations, exported $1.23 million worth of iron ore to the United States in 2024-25, equivalent to 34.96 thousand tons. Australia's role as a major iron ore exporter cements its position as a key supplier to countries like the US.

9. Poland: $273K (5.66 thousand tons)

Poland may not be a significant player in the global iron ore market, but it still managed to supply $273K worth of iron ore to the United States in 2024-25, totaling 5.66 thousand tons. Poland's presence in the US iron ore import market underscores the diverse mix of countries that contribute to meeting the US's iron ore needs.

10. Germany: $48K (1.12 thousand tons)

Germany, a country with a strong industrial base, also played a part in supplying iron ore to the United States, exporting $48K worth of iron ore in 2024-25, amounting to 1.12 thousand tons. Germany's role as an iron ore exporter highlights the interconnected nature of the global steel industry.

List of Top Iron Ore Importers in USA: U.S. Iron Ore Importers & Buyers Database

The US Iron Ore Importers & Buyers Database is a valuable resource for those looking to engage in the iron ore import market. This database compiles information on key companies importing iron ore into the USA, offering insight into market trends and opportunities. The leading & best iron ore importers in the USA, as per the US iron ore importers data & iron ore buyers list for 2024-25, include:

|

Rank |

Company |

Approx. Import Value (2024, $) |

Top Imported Types |

Top Import Sources |

|

1 |

$310 million |

Pellets for DRI & blast furnaces, high-grade fines |

Brazil, Canada |

|

|

2 |

U.S. Steel Corporation |

$190 million |

Pellets, lump ore, blast furnace feed |

Brazil, Canada, Sweden |

|

3 |

Nucor Corporation |

$120 million |

High-grade pellets for DRI plants, limited ore |

Brazil |

|

4 |

ArcelorMittal USA (Cleveland-Cliffs subsidiary) |

$65 million |

Pellets & fines for East Coast plants |

Brazil, Canada |

|

5 |

Steel Dynamics Inc. (SDI) |

$40 million |

Small volumes of ore for DRI feedstock |

Brazil |

|

6 |

Algoma Steel USA operations |

$25 million |

Pellets, occasional fines |

Canada |

|

7 |

Charter Steel |

$20 million |

Ore for specialty steel blending |

Canada, Brazil |

|

8 |

Gerdau Ameristeel (U.S. operations) |

$20 million |

Lump ore and DRI inputs |

Brazil |

|

9 |

AK Steel (subsidiary of Cleveland-Cliffs) |

$15 million |

Pellets, fines for BF operations |

Brazil |

|

10 |

Specialty & niche steelmakers (collective) |

$10 million |

Specialty ores with unique chemistry |

Sweden, South Africa |

Key Insights

-

Cleveland-Cliffs dominates — As the largest integrated steelmaker in the U.S., Cliffs accounts for more than one-third of all U.S. ore imports. Its Toledo DRI plant in Ohio alone requires high-grade Brazilian pellets that domestic mines cannot fully supply.

-

U.S. Steel remains heavily dependent — Despite domestic mining assets, U.S. Steel supplements with imports, particularly Swedish and Brazilian ores that ensure consistent furnace chemistry.

-

Nucor’s selective imports — Though mostly scrap-based, Nucor imports ore and pellets specifically for its Louisiana DRI plant, giving it a small but high-value import footprint.

-

Canada and Brazil supply the bulk — Between them, they account for nearly three-quarters of U.S. iron ore imports, thanks to proximity and quality.

-

Smaller buyers focus on niche needs — Companies like Charter Steel, Gerdau, and specialty mills import relatively small volumes, often of specialty ores not available domestically.

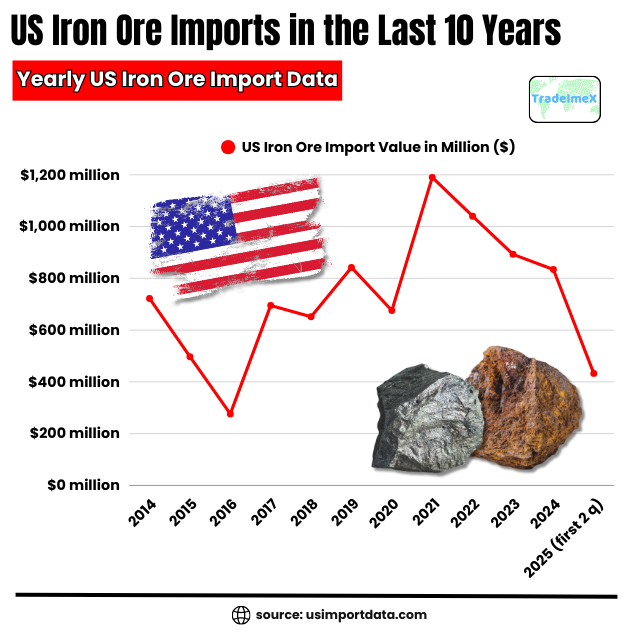

US Iron Ore Imports in the Last 10 Years: Yearly US Iron Ore Import Data

|

Year of Imports |

US Iron Ore Import Value ($) |

|

2014 |

$722.13 million |

|

2015 |

$497.21 million |

|

2016 |

$276.23 million |

|

2017 |

$695.43 million |

|

2018 |

$651.63 million |

|

2019 |

$842.06 million |

|

2020 |

$675.66 million |

|

2021 |

$1.19 billion |

|

2022 |

$1.04 billion |

|

2023 |

$892.68 million |

|

2024 |

$834.20 million |

|

2025 (first 2 quarters) |

$432.81 million |

Who Supplies Iron Ores to the U.S.?

In 2024, the U.S. drew most of its imported iron ore from a narrow group of countries:

-

Brazil remained the largest supplier of raw ore. Brazil’s massive Carajás and Minas Gerais mines produce high-grade ore and pellets ideal for blast furnaces and direct reduction furnaces in the U.S.

-

Canada supplied a substantial share. Canadian mines in Quebec and Labrador ship iron ore south across the border, often in pelletized form, which feeds directly into Midwest steel plants.

-

Sweden and other Nordic producers shipped smaller but critical volumes of specialty ores. These often went to integrated steel producers requiring consistent chemistry.

-

South Africa contributed occasional shipments of lump ore and fines.

Together, Brazil and Canada accounted for over 70 percent of U.S. iron ore imports by value in 2024. The rest was split among a handful of smaller sources.

Where Does the Iron Ore Go in the U.S.?

Iron ore imports are not evenly spread across the U.S. They are concentrated in steelmaking hubs where blast furnaces and direct reduction plants require specific feedstock. Key destinations include:

-

The Great Lakes region — Cleveland, Detroit, and Chicago is home to integrated mills operated by Cleveland-Cliffs and U.S. Steel. These plants rely on both domestic ore from Minnesota’s Mesabi Range and imported ore to balance supply.

-

Louisiana and Texas — These states host direct reduced iron (DRI) facilities that often require high-grade pellets not always available from domestic sources. Imports from Brazil, in particular, supply these plants.

-

East Coast ports — Smaller volumes of iron ore, often from Sweden or Canada, enter through ports like Philadelphia and Baltimore to serve nearby mills.

The geography reflects the close link between logistics costs and competitiveness. Iron ore is heavy and costly to ship; buyers are tightly tied to rail, barge, and port infrastructure.

The Major US Iron Ore Buyers

While official company-level import data is not publicly broken out in detail, industry analysis allows us to identify the main buyers behind U.S. imports:

-

Cleveland-Cliffs

-

The dominant integrated steelmaker in the U.S.

-

Operates blast furnaces in Indiana, Michigan, and Ohio.

-

Also owns pelletizing plants in Minnesota, but still supplements with imported pellets, particularly for its direct reduction plant in Toledo, Ohio.

-

United States Steel Corporation (U.S. Steel)

-

Operates major blast furnace capacity in Indiana and Illinois.

-

Imports select high-grade ores to optimize furnace operations, despite significant domestic mining assets.

-

Nucor Corporation

-

Primarily an electric arc furnace (EAF) steelmaker.

-

Relies heavily on scrap and DRI, not raw ore.

-

Nevertheless, some imports of ore feed its DRI plants in Louisiana and Texas.

-

ArcelorMittal USA (now merged into Cleveland-Cliffs, but still active as a brand)

-

Historically imported ore for its integrated operations, especially on the East Coast.

-

Specialty steelmakers

-

Smaller importers may include producers of stainless or specialty steels requiring niche ores with specific chemistry.

Together, these companies account for nearly all U.S. iron ore imports.

US Iron Ore Import Performance 2024

Breaking down 2024, the numbers show three key trends:

-

Value decline: Import values fell about 6–7 percent compared to 2023, driven by lower global iron ore prices.

-

Volume stability: Import tonnage remained roughly flat, around 4.9 million tons, suggesting that demand from U.S. mills stayed constant, but cost per ton dropped.

-

Premium pricing: Despite the price decline, the U.S. still paid more per ton than most major importers. This reflects smaller volumes, higher reliance on specialty ores, and longer shipping distances in some cases.

Early 2025 Indicators

Through the first half of 2025, U.S. iron ore imports have shown mixed signs:

-

Slight recovery in prices: Benchmark seaborne ore prices rose in early 2025 due to stronger Chinese demand. U.S. import costs rose accordingly.

-

Stable tonnage: U.S. buyers continue to bring in similar volumes, signaling steady steel demand.

-

Growing pig iron imports: Alongside ore, U.S. imports of pig iron, semi-finished iron used by EAF mills, have risen. This suggests steelmakers are diversifying inputs beyond raw ore.

Iron Ore vs. Alternatives

One of the most important dynamics in the U.S. steel sector is the growing reliance on electric arc furnaces, which run primarily on scrap metal rather than iron ore. In 2024, over 70 percent of U.S. steel was produced in EAFs.

This has two implications for imports:

-

Lower overall raw ore demand — U.S. EAF producers do not consume ore directly. Instead, they require scrap, DRI, or pig iron. As a result, the U.S. imports far more of these alternative materials than raw ore.

-

More selective ore demand — The remaining blast furnaces and DRI plants import only the specific ores or pellets they cannot source domestically.

Thus, the role of iron ore imports is narrow but strategic.

Strategic Considerations

Several strategic factors shape U.S. import patterns:

-

Supply chain security: The U.S. government has heightened scrutiny of mineral supply chains. While iron ore is not officially labeled a “critical mineral,” its role in steel production makes supply disruptions politically sensitive.

-

Environmental standards: U.S. buyers increasingly consider the carbon intensity of imported ores. Brazilian high-grade ores have an advantage here, as they enable more efficient steelmaking with lower emissions.

-

Cost competitiveness: With U.S. imports being relatively expensive per ton, companies constantly weigh whether to rely on domestic ore or imports. Logistics costs, tariffs, and exchange rates all matter.

-

Shifts in steel demand: Infrastructure spending, auto production, and energy transition projects (like wind turbines and transmission lines) all shape steel demand, which in turn influences ore imports.

What to Watch in 2025–26

Looking forward, five indicators will determine the trajectory of U.S. iron ore imports:

-

Price trends: If global ore prices continue to rise, U.S. buyers may cut imports or substitute with alternatives.

-

Domestic production: Output from Minnesota’s Mesabi Range and Michigan’s iron ore mines will directly affect the need for imports.

-

EAF expansion: More electric arc furnace capacity means less raw ore demand. However, it also means more demand for DRI and pig iron, some of which require imported ore as feedstock.

-

Brazilian supply stability: Brazil’s role as a top supplier means that disruptions in Brazilian mining or shipping could immediately hit U.S. buyers.

-

Trade policy: Tariffs, quotas, or carbon border adjustments could shift the economics of ore imports.

Conclusion and Final Thoughts

The U.S. is a minor player in global iron ore imports by volume, but not by significance. The roughly $835 million worth of imports in 2024 filled very specific niches in U.S. steelmaking, from high-grade Brazilian pellets to Canadian supplies crossing the border. Imports are concentrated among a handful of large buyers, primarily Cleveland-Cliffs, U.S. Steel, and DRI-operating firms, and are delivered to select regions with strong steelmaking bases.

While 2024 saw a slight dip in value due to softer prices, early 2025 shows stability in demand and a gradual rise in associated materials like pig iron. The long-term trajectory is shaped not by raw ore alone, but by the transformation of the U.S. steel industry toward electric arc furnaces, scrap, and lower-emission feedstocks. The story of US iron ore imports in 2024–25 is therefore not one of scale, but of precision: small but crucial volumes, high costs per ton, and strategic dependence on a few foreign suppliers. As the U.S. steel sector evolves, imports will remain a critical, if narrow, part of the supply chain puzzle.

For more information on the latest US export-import data, or to search live data on US iron ore imports by country, visit USImportdata. Contact us at info@tradeimex.in and get customized US trade reports, market insights, and a verified & exclusive database of the top iron ore importers in the USA, as per your business needs.

What's Your Reaction?